Chicago Fall Market Update

october market update

october market update

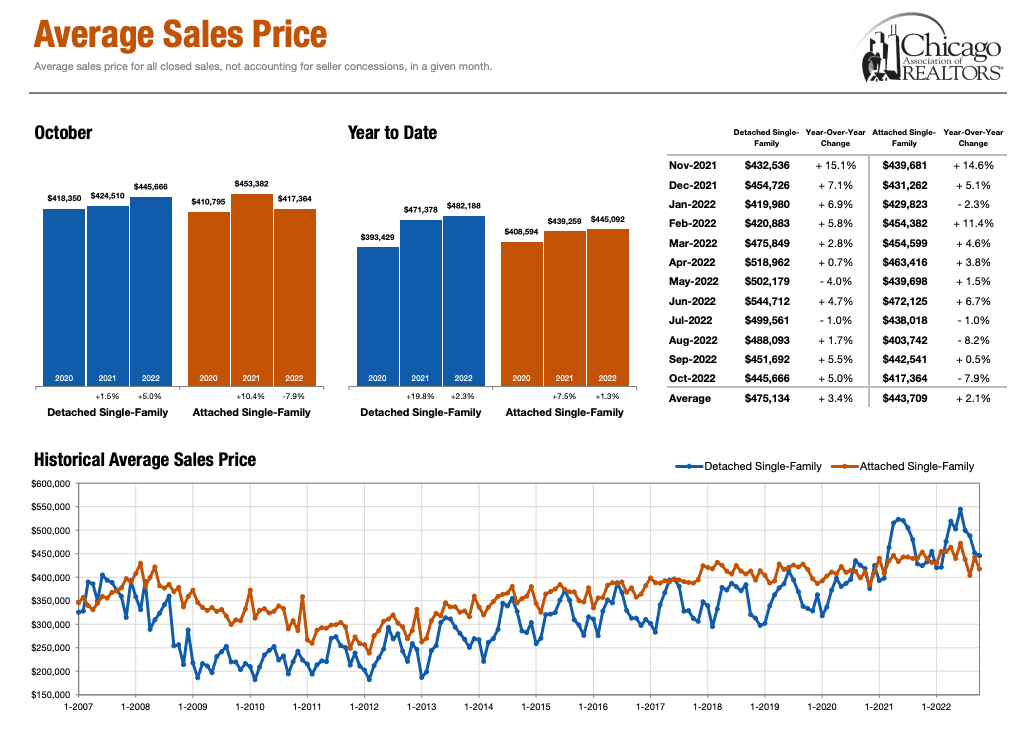

We are starting to see signs of prices coming down in most of Chicago’s housing markets. However, this is primarily due to an uncharacteristically strong fall market in 2021. Average attached single home prices are still up 2.1% on the year and average detached singles are up 3.4% on the year. Detached SFH’s are holding up much better than I had expected, showing strong gains in Aug-Oct. Attached singles, however, have shown weakness over the same period.

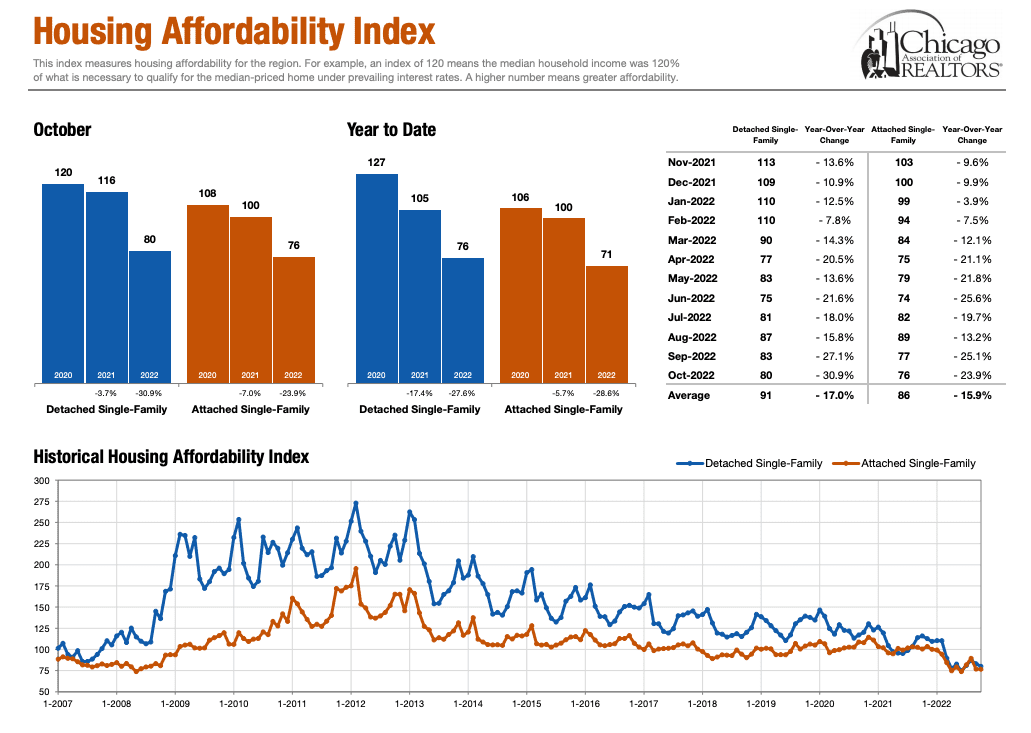

The housing affordability index continues to make new lows going into the month of November. Prices are not coming down nearly as quickly as the cost of debt rises.

I expect that in 2023 we have to see one of two things happen… Rents either need to increase even further, or avg. home prices will need to come down. I know that might seem like a hot take considering how much rents increased in 2021, but rents are still too low. With housing affordability being where it is, more often than not I am finding it is actually more expensive to purchase than it is to rent. The reason being that a lot of sellers don’t need to sell. How long can this hold up? Not sure, but the Chicago market has not seen this relationship between rents and costs of ownership in a very long time. I expect the market will be forced to readjust in 2023.

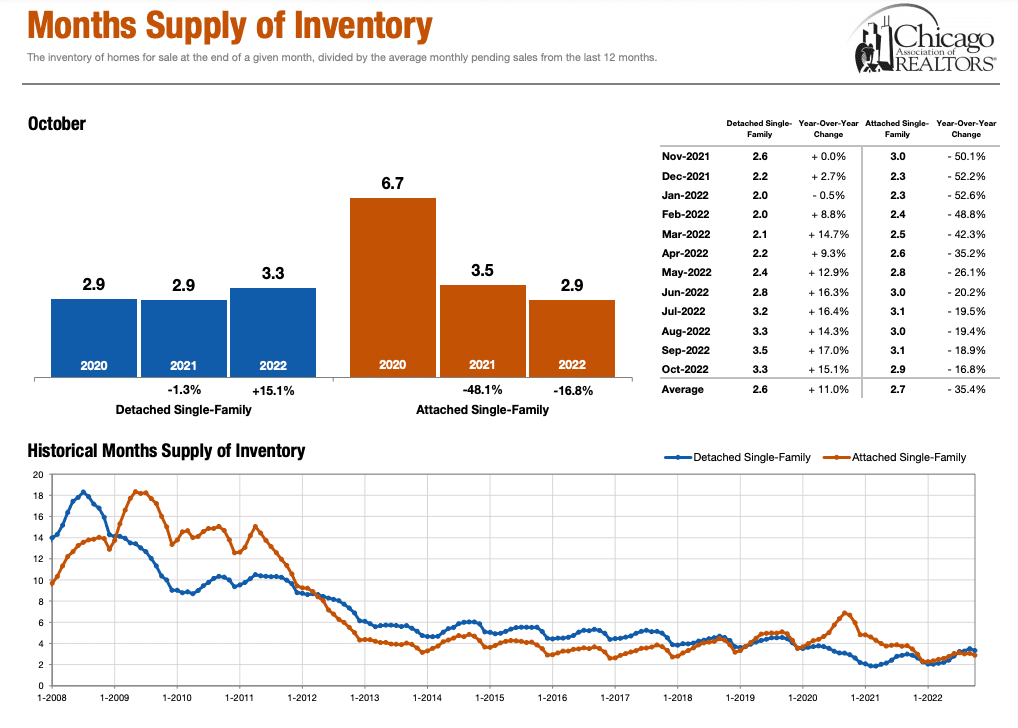

Roughly 25% of residential mortgage holders have a rate below 3%! I am not sure what the exact % of mortgages that are sub 5%, but you can imagine it is pretty high. That is A LOT of inventory that is potentially locked up. It doesn’t make sense for someone to sell out of a low-cost mortgage unless you absolutely have to. More people will choose to remain in properties longer or decide to rent them out as opposed to coming down in price, which is exactly what we are seeing now. Sellers are taking their properties off the sales market in order to rent, and I see this trend potentially continuing through 2023. This will be the biggest challenge in 2023 IMO: Historically low supply in a historically unaffordable market. Not ideal.

If we continue to see historically low supply, which is what I am bracing for, then we can have a situation where home prices stay flat(ish) and rents continue to pick up. That is what I am expecting for 2023. Lower sales volume, flat(ish) prices with downside bias, and higher rents.

There still remain good opportunities in today's housing market. Typically, I recommend planning to hold at least 2-3 years when buying in order to offset the costs associated with transacting. However, in today’s current market I recommend looking to hold 4-5 years and beyond. If that is not doable, then it is important to make sure you purchase something that has solid rentability. You will want to keep your options open.

Most of my buyers who are taking advantage of the low demand right now are buying very, very well. Fall is always the best time to purchase if you want to get a deal, and we are seeing that play out. If you are looking to purchase in Q1 or Q2 of 2023, I would highly recommend getting your ducks in a row sooner than later because it might make sense to start the process before the spring market takes off.

If you are sitting on the sidelines waiting for rates to come down, I think that would be ill-advised. The market has priced in 50 bps for December, which would bring Fed Funds target rate to 4%-4.25%. Historically, mortgage spreads are 1.5%-2% higher, but right now we are seeing 2.5%-3% spreads. If rates come down, I don’t expect them to dip below 6% for all of 2023. As always, you’ll want to consult a mortgage professional for deeper analysis, but this is my personal base case.

It is important to remember that timing the market is challenging and, in my opinion, shouldn't even be an area of focus for the first time home-buyer. It's more important to get rid of your rent obligation altogether. It makes more sense to buy smart by focusing on properties with strong rentability in order to keep your options open as opposed to timing the market. If you try hard enough, you'll always be able to conjure up reasons as to why you shouldn't buy in any given market. Don't be that person who looks back with regret at how much money they wasted renting.

As always, feel free to reach out for a personal consultation whether you plan on looking to buy or rent in 2022 or 2023.

Stay up to date on the latest real estate trends.

Clear cooperation

Quentin Green | November 22, 2024

Quentin Green | September 16, 2024

Quentin Green | September 10, 2024

Quentin Green | August 26, 2024

Quentin Green | August 19, 2024

Quentin Green | July 29, 2024

Quentin Green | July 26, 2024

rent control

Quentin Green | July 17, 2024

summer shift

Quentin Green | June 11, 2024

Chicago Real Estate market update

Long on going relationships are the reason I love this job so much. Being able to see someone's face light up as I hand them the keys to their very first house is what gets me up in the morning.