How did everyone get 2022 mortgage rates so wrong? And what to expect for mortgage rates in 2023.

mortgage rates

mortgage rates

I never paid too much attention to mortgage rates until earlier this year if I am being completely honest. I always thought of it as ”it is what it is'' since they’re out of our control. I would always defer to lenders with anything mortgage related. That is still how I tend to navigate a lot of those conversations, but mortgage markets have become more of a core focus of mine recently. In late 2021/early 2022, I noticed that the vast majority of lenders I spoke to were anticipating rates going no higher than 4%! At the time, I thought this was bizarre because asset prices were overly inflated and showed no signs of easing, and I expected that what was happening to asset prices would eventually happen to everything else. If clients asked me what type of mortgage they should get, I always recommended a 30-year fixed, as opposed to 15-year fixed or an ARM, just because it seemed too good to be true.

I have been hearing a lot of chatter about rates coming down. It is true, rates have been coming down over the past couple months. This is due to strong performance from the 10-year treasury and also mortgage spreads compressing after having been historically wide for all of 2022. To be clear, they still are historically wide today. A lot of people I like and respect are anticipating sub 6% rates before Q2 of 2023, but I am not sure I'm sold on that happening in 2023. Although I can certainly see a path to sub 6% mortgage rates (more on that later), I can also see a situation where the Fed goes against the markets and holds rates higher for longer. Later on, I will talk about why I think there is a decent chance that the Fed doesn’t cut rates through all of 2023. Not what you want to hear, I know.

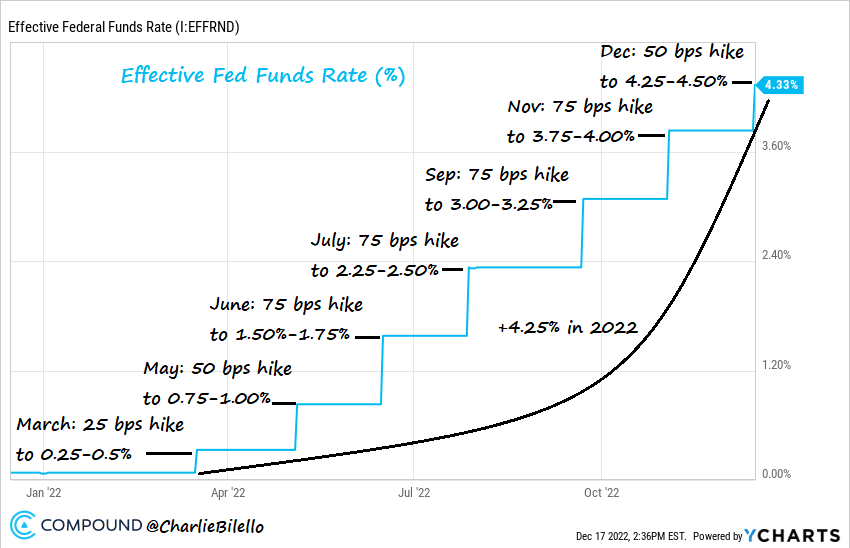

See below chart by Charlie Bilello. Charlie is a RE Macro guy who has an awesome newsletter I subscribe to. Highly recommend subscribing if you are into that kind of stuff, like I am.

This chart shows fed funds rate hikes dating back to March of ‘22. These are not mortgage rates. The Fed funds rate is actually further removed from mortgage rates than people think. The Fed funds rate influences short term interest rates most directly (think short dated treasuries less than 2 years). But it is the 10-year treasury that is most directly tied to mortgage rates. For example, as of 12/21/22 the Fed funds rate sits at 4.25%-4.5%, but the 10 year treasury note is at 3.665%. This just means that the markets are anticipating lower inflation and lower rates over a 10-year backdrop. Typically, mortgage rates are 1.5%-2% more than the 10-year, so in a normal environment we would expect mortgage rates to be at 5.15%-5.65%.

The terminal fed funds rate (what experts predict will be the highest fed funds rate in a hiking cycle) is now sitting at about 4.85%-5.1%. Powell has been incredibly hawkish and has been indicating to the market, in my opinion, that he has no plans to cut rates in 2023. In other words, he's not thinking about thinking about cutting rates. We've heard that before. Well the bond markets disagree with him and are pricing in rate cuts towards the middle of 2023. The markets are telling Powell that something will happen (could be higher than anticipated disinflation, credit shock, etc.) that will force the Fed to cut rates. But what if Powell is right this time?

To play devil's advocate, I have laid out a couple of paths to sub 6% mortgage rates: 1.) We see further disinflation and possibly deflation in the economy and massive layoffs (RECESSION), which leads the Fed to believe the job has been done and puts them on a path to easing rates. 2.) We see such a huge deflationary shock in credit markets that will also force the Fed to ease rates. In both scenarios, you should see the Fed funds rate come down, 10 year treasury yields come down, then mortgage rates should follow. On top of this, the markets could gain more certainty in that rates must remain lower for longer, which means mortgage spreads can tighten (Mortgage spreads probably tighten more in scenario 1 versus scenario 2). These 2 scenarios combined are actually the consensus opinion: Something deflationary will happen to force the Fed to pivot course.

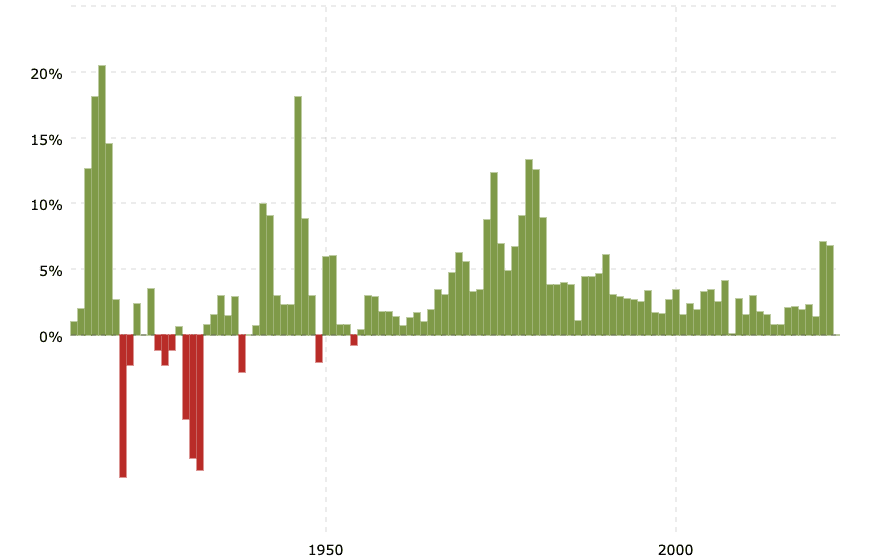

Now here is why I think people might be wrong about interest rates dipping below 6% in 2023. See chart below tracking inflation dating back to 1940. What do you notice? I’ll tell you what I see: double tops in inflation for periods of historically high inflation. The Fed knows this, which is why I think we could see rates higher for longer. Think about it… It’s not worth the risk for the Fed to pivot early and get inflation wrong AGAIN, especially considering the “temporary” inflation mess they didn’t see coming in the first place.

I don’t take pleasure in bashing the Fed, and I certainly don’t envy their job. So EVEN IF it actually is different this time, and I think there may be a good argument that it might be, it is important to realize the Fed is both backward and forward looking. They know the risks of pivoting too early, as shown above. It’s not about what the Fed should do, it’s about what the Fed WILL DO. Remember that.

To be clear, I am not saying that this will happen. I am saying that this seems like a mispriced scenario in the market, meaning that I find there may be a higher probability of this happening than what the market probability assigns to it.

Most experts expect to see rate cuts in the middle/second half of 2023. The Fed likely doesn’t actually need to raise rates too much higher in order to fully fight inflation, but they may need to hold rates higher for longer in order to convince themselves that they have sufficiently fought back inflation. This path makes sense to me because 1.) It restores Fed credibility, and 2.) It helps ensure we don’t have a double top in inflation. For now, this is my base case until I begin to see things that will make me think differently. Or until the Fed breaks something so bad that will require a pivot, at which point we will have bigger problems on our hands.

I have also included a link below to a podcast I frequently listen to. I agree with a lot of what they talk about here. Worth a listen! They sort of come to this "Ah ha" moment around 52:00 minutes in where they discuss a situation in which new construction could become much more price sensitive relative to existing construction because of the financing dynamics and supply of new construction. Because most people with existing homes have mortgage rates between 3% and 5% and the majority of new construction buyers tend to be step-up buyers rather than first-time home buyers, developers might find them in a situation where they need to cut prices low enough to convince the step-up buyer to ditch their sub 5% mortgage and sign up for a 6%-7% mortgage. Additionally, we are seeing incredibly low supply (about 500,000) homes on the market right now. In comparison, we typically see around 1M homes on the market at any given time, and of that 1M about 10% is typically new construction. The problem is, we are expecting about 150,000-200,000 new construction homes in the first month of 2023. With the already tight inventory, the % of new construction homes would actually be closer to 40%, which could create a nice buying opportunity for new construction homes. That is where you might see real price discovery. This makes a lot of sense to me, and it is something I had not thought about until now.

What the Real Estate Market Will Look Like in 2023

That is all for now. Not many actionable takeaways here, but I just wanted to share my thoughts as this is what I am preparing for. My next market update will be in early Jan, and I will go over the November data. I will probably skip December altogether just because of Holidays and slow seasonality.

As always, please reach out if you are planning to buy/sell/rent in 2023. Or if you just have general questions and want to talk RE.

Stay up to date on the latest real estate trends.

Clear cooperation

Quentin Green | November 22, 2024

Quentin Green | September 16, 2024

Quentin Green | September 10, 2024

Quentin Green | August 26, 2024

Quentin Green | August 19, 2024

Quentin Green | July 29, 2024

Quentin Green | July 26, 2024

rent control

Quentin Green | July 17, 2024

summer shift

Quentin Green | June 11, 2024

Chicago Real Estate market update

Long on going relationships are the reason I love this job so much. Being able to see someone's face light up as I hand them the keys to their very first house is what gets me up in the morning.