January Market Update

housing affordability

housing affordability

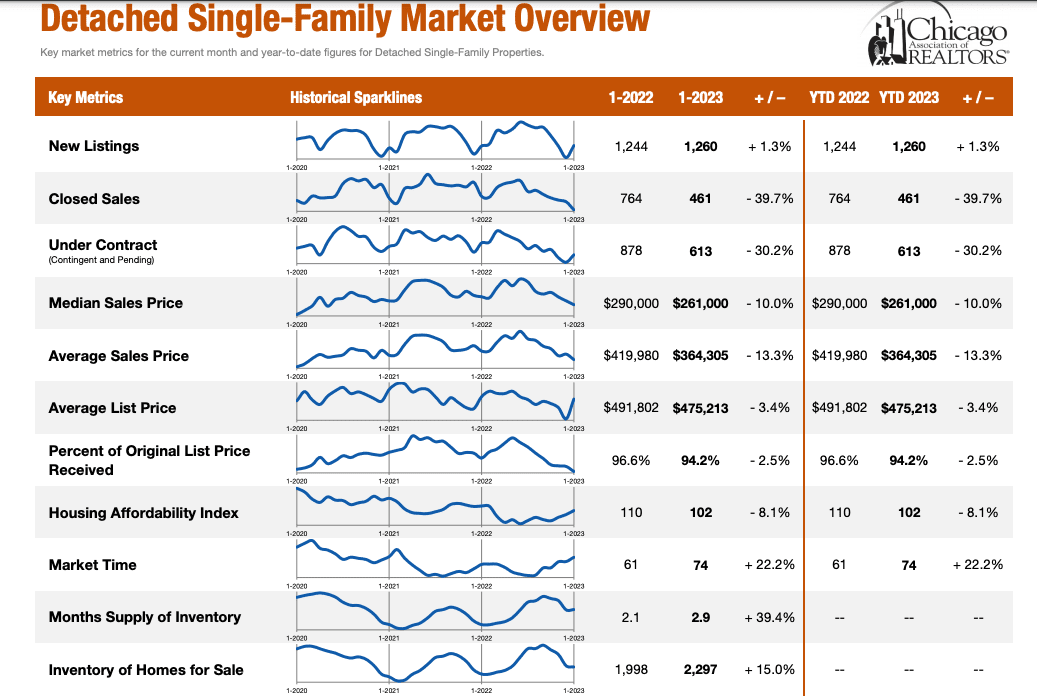

January numbers are out. Hate to say that the year is playing out exactly as I had expected, but so far it is. Inventory is down 11% YOY and home sales are down a whopping 41% YOY. I expect this year to continue on its trend of low inventory and even lower sales volume.

We are seeing some softening in the detached SFH’s in Chicago. Inventory is up slightly, while closed sales are down significantly. See graph below. Even with inventory being where it is, the demand is coming in softer than people had expected. Supply is still sitting at 2.9 months, which is up from 2.1 months. Still a sellers market, but that is a sizable increase in supply worth paying attention to.

January and February are both transition months, so take this data with a grain of salt and remember Q1 of 2022 was bonkers in Chicago. However, if we continue to see more supply, then expect that to negatively impact housing prices.

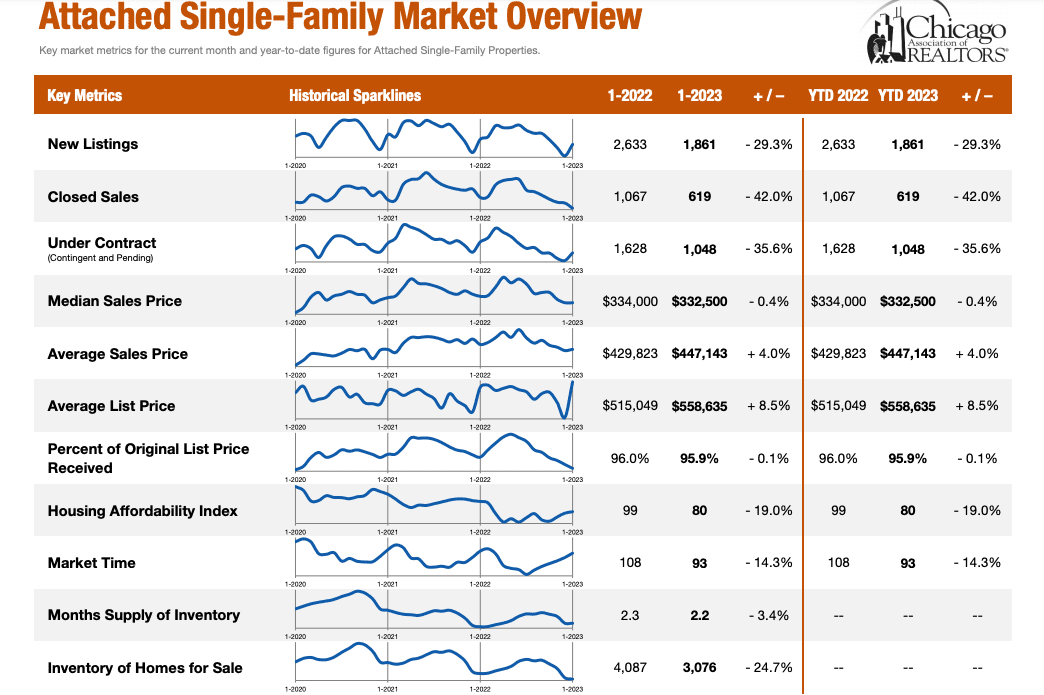

Condos continue to outperform relative to SFH’s. Although both new listing and closed sales are down significantly, prices are stable and gradually increasing. Again, this makes sense considering how poorly condos, especially downtown condos, underperformed in 2021-2022.

If you are a downtown condo owner, you have to be happy with these numbers. I think it is highly likely that the downtown condo market has bottomed out and things are finally normalizing.

I cannot stress enough how different the various markets are in Chicago. It’s hard to believe, but the SFH market and condo market have been basically doing the opposite of one another going back to the start of Covid. However, if there is one thing in common, it’s demand. Closed sales and under contract are down significantly for both SFH’s and condos. That paints a completely different demand picture to that of Q1 of 2022 (so far).

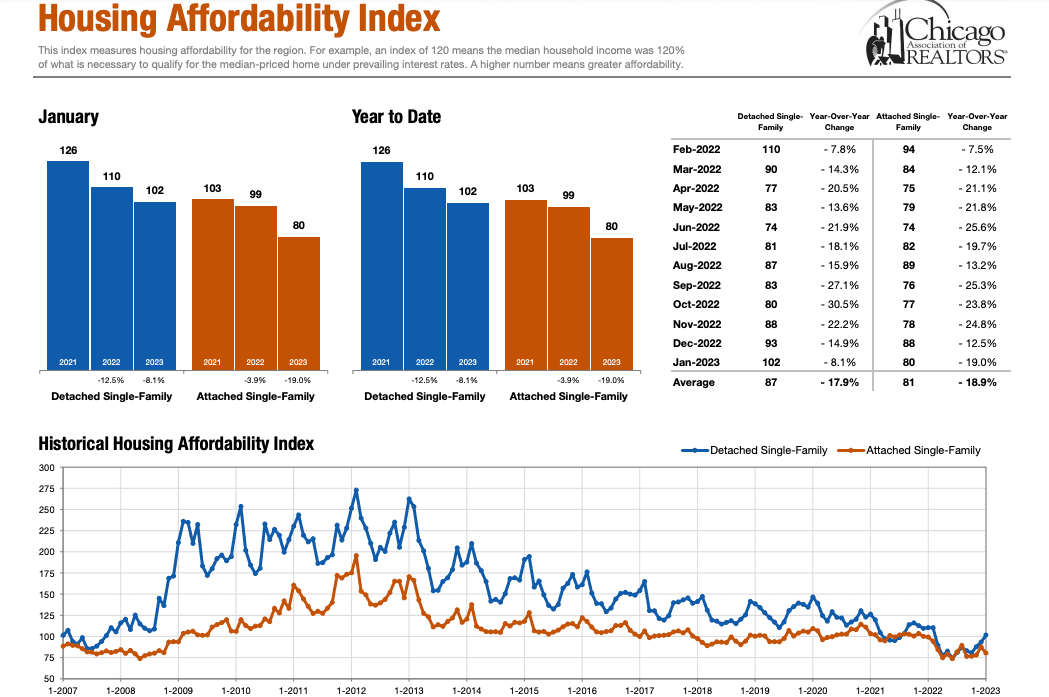

Housing affordability is continuing to hurt the consumer. A healthy housing affordability index is generally above 100. The higher the better. This number is moving lower YOY dating back to 2021. You can blame J Powell for that. The consumer is getting squeezed big time and something will have to give. Expect rents to increase because of this.

As always, please reach out if you have any questions or are looking to buy/sell/rent in 2023. I am here to help and advise in any way possible. Keep in mind that the Chicago market is composed of countless submarkets that operate differently. You can only learn so much from this data, so please reach out if you would like a more precise market overview for a specific area.

Stay up to date on the latest real estate trends.

Clear cooperation

Quentin Green | November 22, 2024

Quentin Green | September 16, 2024

Quentin Green | September 10, 2024

Quentin Green | August 26, 2024

Quentin Green | August 19, 2024

Quentin Green | July 29, 2024

Quentin Green | July 26, 2024

rent control

Quentin Green | July 17, 2024

summer shift

Quentin Green | June 11, 2024

Chicago Real Estate market update

Long on going relationships are the reason I love this job so much. Being able to see someone's face light up as I hand them the keys to their very first house is what gets me up in the morning.