Key takeaways from Straight Up Chicago Investor podcast ft. J Scott with Bigger Pockets

overblown housing recession

overblown housing recession

There is a ton to unpack here, so I definitely recommend giving this episode your full attention, but here are some quick takeaways. I left a lot of great information out and wanted to focus primarily on actionable items. Link to listen to the actual podcast is here >> Straight Up Chicago Investor Podcast

Let's dive in... We have been in a rate hiking cycle since March, but what exactly happens to the economy when you raise rates? Everything basically becomes more expensive because the cost of debt increases, which in turn incentivizes people to save. This means that demand in the economy drops, and when demand drops, prices also come down as companies cut costs. This in turn should reduce inflation. It’s a bit more complicated than that, but you get the gist.

J points out that there are two ways to go about raising rates: You can either raise them quickly to stamp out inflation, or you can raise them gradually over a longer time horizon. What is Powell doing? Since this rate-cycle began, he has been gradually raising rates over a longer time-horizon and has signaled to the market that he plans to continue on with this approach. What's the problem there? You will likely enter a situation with high rates AND high inflation for a period of time, which is exactly what we are seeing now! It’s the worst of both worlds. Conversely, the problem with raising rates too quickly is that it sends the debt market into spirals, which can have more immediate and significant adverse effects on the economy as a whole. Bottom line: Inflation is sticky, and there is no easy way to get out of it. There is really no great way to tackle inflation without doing serious damage to the economy. The good thing is that we seem to know the Fed’s playbook. Now we just have to unpack all that in order to figure out what this means for RE.

Typically, rate-hiking cycles last up to 18 months, which means we could start to see credit ease again sometime before September 2023. Is it likely prices continue to slide until the rate-cycle is over? Sure, but I wouldn’t let that necessarily stop you from being active in this market. I am in complete agreement that if you are buying with the intention of holding, it will still probably make sense, ESPECIALLY if you are currently renting. Not going into the rent vs. buy scenario, but bottom line is you’ll likely lose money if you plan to rent for more than 2-3 years as opposed to buying. If you are speculating or flipping in this type of market, just be prepared and know what you are signing up for because we likely won’t see growth in most markets over the next 12 months.

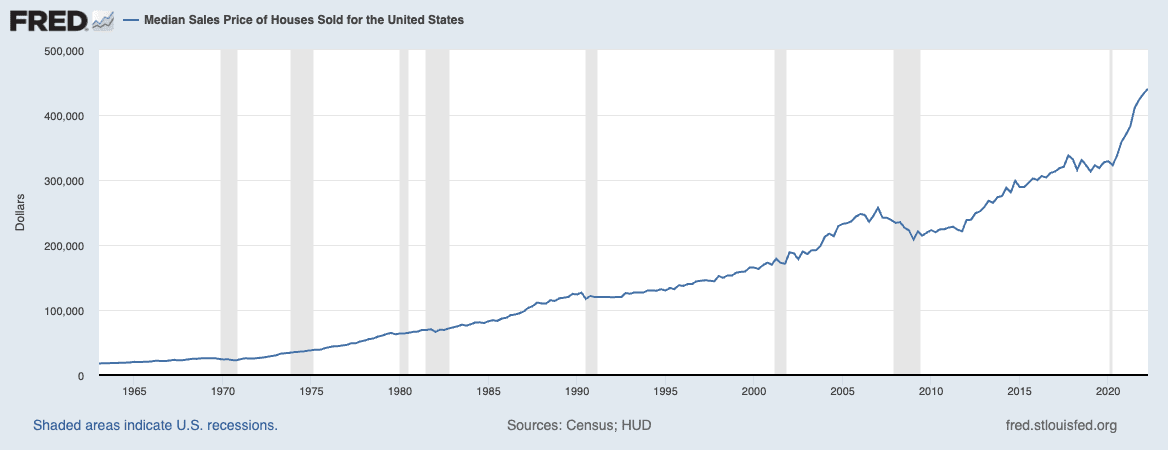

J predicts the overall housing market won’t get hit as bad as it did in 08. This is the consensus expert opinion, which I agree with for a few reasons, but the following sums it up pretty well. We have had 35 recessions in the past 160 years, which is 1 every 5 years. The RE market got smacked only twice within that timeframe due to recession, which was 2008 and the great recession in 1928. I was somewhat surprised when I heard this so decided to do some additional research just to confirm, and J is right on the money. So statistically, there is a very favorable chance RE will not get hit as hard as people think. This is such a key takeaway because the last recession we had created the worst environment we have ever seen for RE, which is why it seems like almost everyone thinks the RE market is going to implode like it did last time. It’s OVERBLOWN.

I pulled this chart from the St Louis Fed. The gray lines above represent recessions dating back to 1960. So from 1960, we had a recession about every 7.5 years, depending on whether you count 2020 as a recession or not. But as you can see, there is really no statistically significant decline in home prices besides 2008!

Another key point is that the debt market is becoming tighter and will continue to contract, which means access to capital will become more difficult. This will persist until the Fed has done its job to ease inflation. And if you are someone who thinks the Fed will pivot when the economy cries “uncle” then best of luck to you. It’s not likely, and the markets are starting to realize that.

What can you do now to prepare for this? If you have something that needs to be refinanced within a year from now, it might make more sense to refinance now before lending standards get tighter so talk to your lender and see what they can do for you.

Now is the time to build your credit… Get your ducks in line before it becomes harder to access capital. I’ve been telling my clients for years that they should always be extending their credit limit to the absolute maximum in order to minimize their debt to income ratios. There are tons of things you can be doing now to build your credit that I won’t go into, but here is a good link I would recommend–https://www.biggerpockets.com/blog/how-to-build-credit.

I was not around in 2008, but it was very difficult to access capital for RE if you had a credit score of under 740. Now you can get a loan for as low as 540, and I have read articles about certain banks lending against even lower credit without putting any money down. It’s hard to imagine that will continue.

CEO sentiment as an indicator… Great tidbit of info here and something I will absolutely be watching more closely in the future. The importance of CEO sentiment cannot be overstated because of the effect CEO’s have on the economy through their decision-making process. If CEO’s think the economy is going one way or another, then they will allocate capital in order to align with their market view that will either slow down or speed up the economy. They almost create the very market conditions they are anticipating regardless of whether they are right or wrong. I think a lot of people focus on consumer sentiment as an economic indicator, but CEO sentiment, in my opinion, may be just as important.

My personal BIGGEST TAKEAWAY from this episode: The idea of looking at debt instruments as assets. J could not be more spot on when he says “the house is no longer the asset, the loan is the asset”, and for a short time that was the case. Most people never thought rates could even get that low… It was a truly unique situation and hats off to anyone who secured RE or debt with rates in the sub 4’s or even sub 5’s. For anyone in that camp, YOU SHOULD SERIOUSLY CONSIDER HOLDING ONTO WHATEVER RE YOU OWN. Instead of selling, get creative and seriously consider renting in some form or fashion if that is an option for you. Even when you factor in management fees, it will be well worth it because of how valuable your loan structure is. I’m in complete agreement with J in that the best way to create true wealth in RE is buy and hold. Cash flow and appreciation are great, but debt reduction is just easier for the everyday person because all you have to do is pay it down over a 30 year time horizon and BAM you have a nice little retirement account with your name on it. Even if you own a rental that is not making a ton of money in cash flows, the leverage against your RE can allow you to make 5%-7% a year JUST THROUGH DEBT REDUCTION. That is not even including the tax benefits, appreciation, and cash flow… There is no other asset class that compares to RE when you look at it from this lens.

What do you need to watch out for in the coming 12-18 months? Supply will be the biggest factor IMO. I think a lot of supply will stay off the market for some time because so many people were able to purchase and refinance debt at historically low rates. It doesn't make sense to lose out on this financing, which means that people will be less incentivized to sell. And let's face it, people just are not in a position to be forced to sell right now. The average homeowner has over 25% in home equity from 2 years ago, which means we will need to see prices come down substantially in order to see the short sales and foreclosures from 2008 that drove the RE market into turmoil. It's hard to imagine. Regardless, supply is the most important indicator to watch over the next 12 months.

Secondly, it is important to keep in mind that the general consensus is that this rate-hiking cycle will last less than 18 months from March of 2022. What happens if we are in an extended cycle where the Fed raises rates for longer? It's not clear, but it would be a bad sign for RE as a whole. Keep an eye on core inflation data and the Fed since they have made it clear that they will not ease up until inflation is back at normal levels.

Final thoughts: It is incredibly important to stay nimble and understand what is affecting current market conditions. If you have a firm understanding of that, then you will be able to better predict future market conditions. There is always opportunity in any market no matter how bad the conditions. It is up to you to figure out what is mispriced and how to benefit from it. What works this year might not work 6 months or a year from now. Savvy investors are constantly absorbing new information and applying this to their overall macro outlook, which keeps them ahead of the crowd. There is always something you can do to maximize profits and minimize risks.

Stay up to date on the latest real estate trends.

Clear cooperation

Quentin Green | November 22, 2024

Quentin Green | September 16, 2024

Quentin Green | September 10, 2024

Quentin Green | August 26, 2024

Quentin Green | August 19, 2024

Quentin Green | July 29, 2024

Quentin Green | July 26, 2024

rent control

Quentin Green | July 17, 2024

summer shift

Quentin Green | June 11, 2024

Chicago Real Estate market update

Long on going relationships are the reason I love this job so much. Being able to see someone's face light up as I hand them the keys to their very first house is what gets me up in the morning.