Reasons for opportunistic buyers to consider buying properties in 2024

Chicago market update

Chicago market update

January is officially in the books, and boy did it fly by. Overall, it seems to feel like the market has a fresh sense of energy to it that we haven’t seen in some time. Most of the buyers I am talking to now are excited and eager to get started in the home buying process. The beginning of 2023 was the exact opposite. I am calling 2023 the year of the “reluctant buyer”.

Do you rent or buy? This is the question that potential first time homebuyers battle with every year. In 2023, a larger % of my clients were keeping both renting and buying options open throughout the entire process. Whether or not someone decided to rent or buy was very case by case. More people were renting and more people were backing out of deals. Buying a home for the first time can be an incredibly exciting achievement, but I noticed that a lot of buyers were just less excited and more reluctant than in the past.

This makes a lot of sense when you look back at what happened in 2023. We saw 8 rate hikes throughout the year, and it wasn’t until late October when rates finally began to ease up. Below is a graph tracking the 30 year mortgage rates from Jan 2023 to Jan 2024.

One thing I pride myself on is being brutally honest with my clients. The reality was that it just made more sense for a lot of people to rent versus buy in 2023. Affordability declined as the year went on as we saw both prices and interest rates inch higher. Rents continued to inch up as well, but they didn’t go up as much as affordability went down so you just saw more first time homebuyers punting.

2024 should be a very different year. Although interest rates are starting out higher than where they were in January of 2023, we should see rates gradually come down throughout the year. This will offer continuous relief for the first time home buyer and should impact demand positively throughout the year, which is why a lot of forecasters are calling for prices at a national level to increase anywhere from 2% to 10%. Very few forecasters are anticipating national prices to come down.

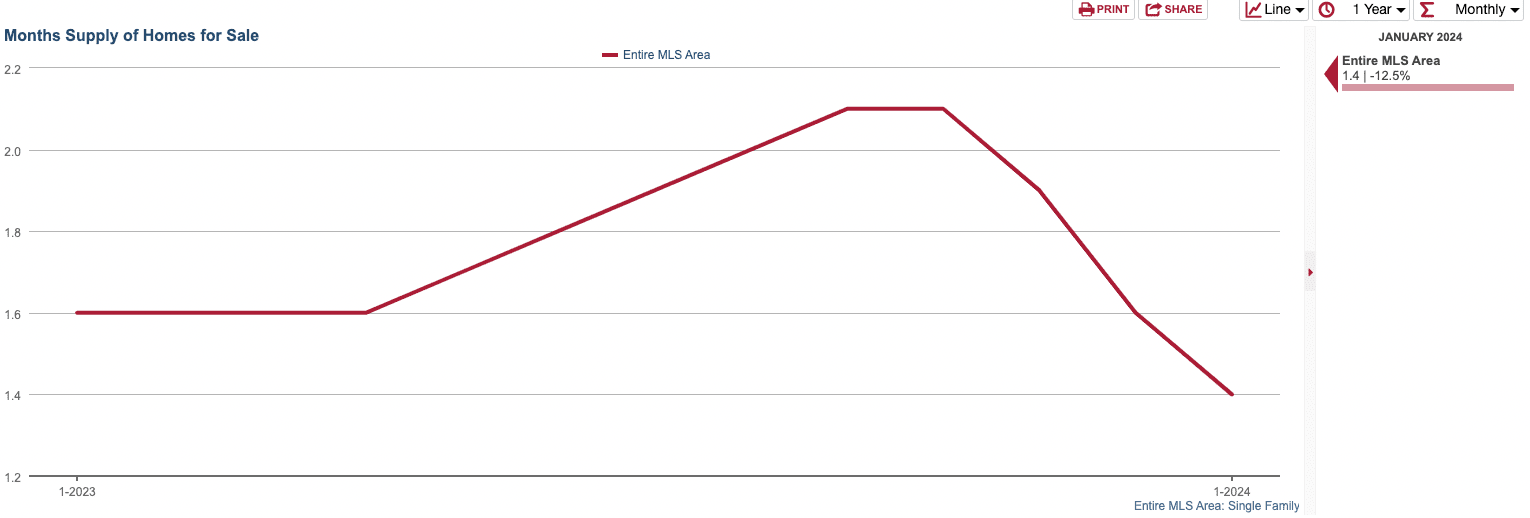

Although there is a lot to be excited about for 2023, we are still dealing with a severe inventory shortage. A lot of the excitement out there, especially from other real estate professionals, seems to be more qualitative than quantitative. The chart below shows month's supply in Chicago from 2023 to 2024. As you can see, we are starting the year with less supply than we were in 2023. This is one of the reasons why I think Chicago will outperform in 2024 just like it did in 2023.

Mortgage application data is a great way to predict inventory. Sellers are generally buyers, and they almost always go through the mortgage process prior to listing their home. So if mortgage apps go up, then you can expect inventory to follow. This is why inventory is very predictable. Very few people sell and then rent, so it’s very rare to see inventory shocks. The below screenshot is the Mortgage market index going back to Jan 2023. As you can see, we are starting off the year similarly to how we did in 2024.

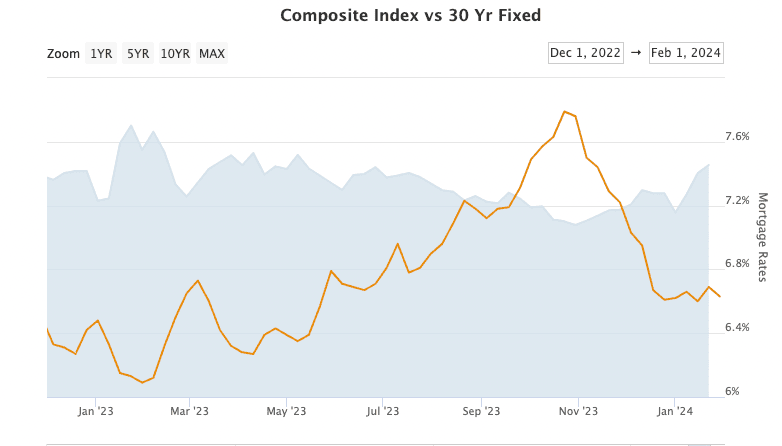

There is some good news! What is different about 2023 versus 2024 is that we finally have some tailwinds behind us. The below chart shows 30 year mortgage rates against the backdrop of the mortgage market index. They are inversely related. Rates go down, mortgage apps go up and vice versa.

Assuming that we continue to see rates come down, then we should see inventory and demand pick up with it. Whether or not demand will outstrip inventory is an entirely different conversation.

Nonetheless, I think that the consumer will feel a lot better going into this year as compared to 2023. We’ve seen the stock market rip since October AND we have seen rates come down by over 1 basis point. This is huge for the consumer, especially at the onset of a new year.

What does all of this mean for buyers? It’s going to be a very competitive Q1 and Q2. If you are buying in the spring, you have to go into it knowing that it will be ultra competitive. More competitive than it was last year. However, I think the late summer/fall will be a great time to buy. If things play out how I expect them to, then we should be in a market with lower interest rates (sub 6.5%), and much higher inventory. This would be the first time in a while where we could be entering a fall market with both declining rates and higher than previous years' inventory, so get ready! We are also going to be in the middle of election season. People are generally more risk averse during election years.

Here is a breakdown of what we are seeing in most of the markets:

Lincoln Park/ Old Town (60614):

Lakeview (60657)

West Loop (60607)

West Town (60622)

Wicker/Buck/Logan (60647 and 60642)

South Loop (60605 and 60616)

Loop/LakeShore East

River North

Streeterville

Gold Coast

Stay up to date on the latest real estate trends.

Clear cooperation

Quentin Green | November 22, 2024

Quentin Green | September 16, 2024

Quentin Green | September 10, 2024

Quentin Green | August 26, 2024

Quentin Green | August 19, 2024

Quentin Green | July 29, 2024

Quentin Green | July 26, 2024

rent control

Quentin Green | July 17, 2024

summer shift

Quentin Green | June 11, 2024

Chicago Real Estate market update

Long on going relationships are the reason I love this job so much. Being able to see someone's face light up as I hand them the keys to their very first house is what gets me up in the morning.